Ted Spradlin

Ted Spradlin

Fix and Flip Loans — Mortgage Funds Versus Conduit Lenders

Real estate investors have their choice of several private money lenders to help them acquire and renovate their next fix and flip project. However,...

If you’re applying for private money financing to renovate a property, you’ll want to prepare all the fix and flip loan application requirements to submit for underwriting. Having your financial and business documents in order will help you stand out among the crowd. Most borrowers aren’t highly organized and can't promptly send documents upon request. They're working on projects and not sitting in front of a computer all day.

If you want your loan approved faster with fewer back and forth requests for documents, budgets, and other items, get organized so the people who do sit in front of computers — mortgage brokers, lenders, and title and escrow officers — can push your loan through quickly so you can get started.

This article will cover the fix and flip loan application requirements that you need to prepare before applying for financing.

Not all the items will necessarily apply to your situation. However, it’s wise to know what might be requested so you can have that document ready to go.

Before we delve into the application requirements, I want to explain the different types of lenders offering fix and flip loans. Each has a different source of capital — individual funds, principals, fund investors, or bank credit facilities — which necessitate different loan requirements.

A private individual lending their own money against a fix and flip project will most likely require the least amount of documentation. They're lending against the value of the hard asset — the real estate — with little consideration to other personal financial information.

The family offices and real estate offices FCTD regularly works with want to know their potential borrower very well. Since their capital comes from a combination of principal and family member money (along with bank credit facilities) this includes a good credit check, a clean background, and documented experience for their credit file.

A mortgage fund is a pooled investment entity run by a fund manager, or general partner (GP) on behalf of the fund investors, or limited partners (LPs). Per the partnership agreement, GPs have fiduciary responsibilities to the LPs to underwrite loans to a specified level, by verifying credit, background, and liquidity. Some mortgage funds have bank credit lines that also require loan-level underwriting documents for the credit file.

Conduit fix and flip lenders originate loans they sell to investors in the secondary market, such as hedge funds, pension managers, or other investors. Both conduit lenders and the investors who buy their loans often use credit facilities with covenants requiring specific loan-level documentation. Though conduit lenders have the most stringent requirements, they’re also the leading source of fix and flip capital in the marketplace.

Even if you’re acquiring a property in an LLC or corporation, private money and hard money lenders will want a loan application for you and your entity, such as the one above, which provides important identifying information that will be used by the lender and title company.

The application, with authorizations to run credit and background checks, allow the fix and flip lender to underwrite the loan, ensuring that you’re a smart credit risk who can perform and repay the loan.

Fix and flip private money lenders will almost always check a borrowers credit, looking for good to great credit scores. A good or average credit score is 640-680, which usually signifies some maxed-out or almost maxed-out credit cards and revolving accounts. A score of 680-720 reflects some balances on the credit report, but nothing that raises red flags. Over 720 FICO scores are best.

It’s hard to find fix and flip lenders that will finance a borrower with bad credit in the 500-600 range. Maybe a private individual lender would consider it, but not a conduit lender or a mortgage fund holding the loan on their books.

Background checks fill in the information gaps that credit reports leave out, including arrest records; mug shots; financial crimes, unpaid business and personal tax liens; foreclosures from properties held in entities or financed by private money loans; and much more. The background check can also verify the properties you listed in your proof of experience.

A best practice is to store documentation in a folder on your computer or mobile device so you can quickly access and submit them.

Both the front and back of the driver’s license is needed.

Family and real estate offices, mortgage funds, and conduit lenders almost always want to see 2-6 months of business and personal bank statements. It proves what’s coming in and going out, and alerts them if there is a pattern of overdrafts.

Lenders look for sufficient cash on-hand for down payment and closing costs. Additionally, they look for post-close liquidity to make sure you can service the debt and cover utilities and property taxes.

Conduit lenders often ask for one year of business and personal tax returns to ensure the borrower is filing taxes. (FCTD has had situations where borrowers hadn’t filed income tax returns in five years. This was a red flag — and we didn't proceed.)

If you’re acquiring a property in an LLC or corporation, you’ll need to provide the Articles, Bylaws or Operating Agreement, as well as the EIN, to be verified by the lender and title company.

***Make sure your entity is in good standing with the secretary of state’s office***

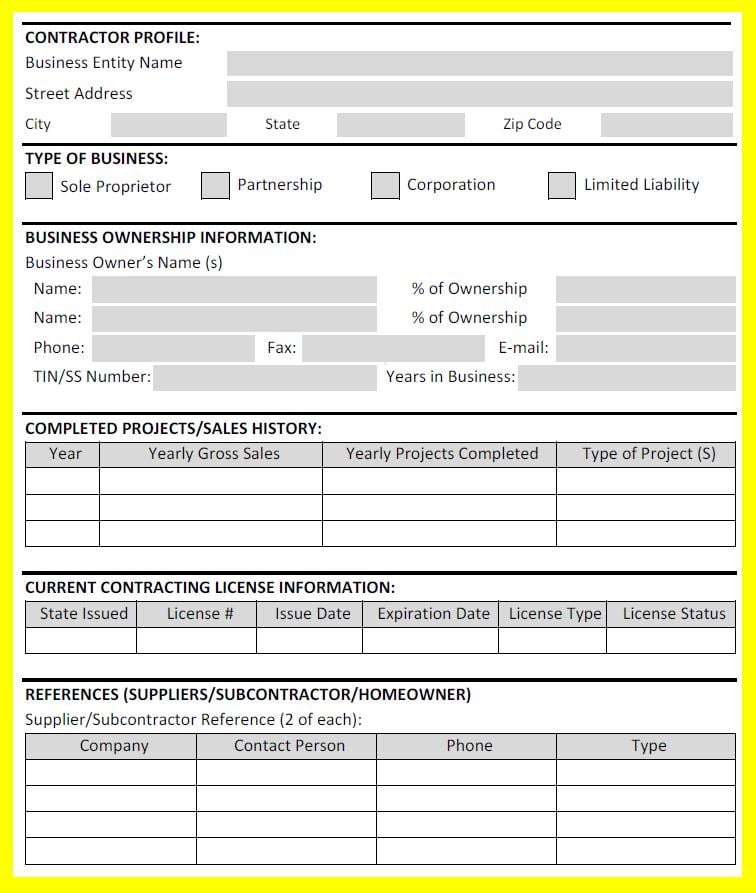

If you’re applying for rehab financing, the lender will do a GC review of your general contractor. The GC may be you, which means that you’d fill out the contractor profile and provide supporting paperwork, including license, insurance, and entity documents.

You'll need to send documentation related to the property and transaction information.

You'll provide the sale agreement, including all addendums. Transactions get held up when addendums are missing or not signed by one party.

Private money lenders must comply with anti-money laundering laws (AML), so you’ll need to submit a copy of the EMD receipt. If you wired the EMD, provide the receipt plus a screenshot of the transaction history from your bank account, showing the wire to the title company. If you wrote a check, supply a copy of the cancelled check or cashier’s check.

You may only have the escrow officer's contact info, which is fine. They can provide the title company details.

It’s smart to send over the insurance agent information early in the transaction. Some insurance companies won’t insure fix and flip projects, so it’s best to get confirmation of coverage early rather than at the eleventh hour.

For experienced rehabbers, submitting the property information is probably the easiest part of the process since this is your area of expertise.

Lenders require a detailed rehab budget, which they'll internally review and send to the appraiser to factor in the After Repair Value (ARV).

The budget will help determine the number of required construction draws. Most fix and flip projects have between 2-5 construction draws, depending on the size of the project.

You’ll need to submit plans for a new addition or changes to the layout.

Summary

Each type of private lender is going to have a different set of requirements. Individual trust deed investors will need the least, while conduit fix and flip lenders will need lots of documentation.

Either way, when you're highly organized with your fix and flip application requirements, your loan can move quickly through the underwriting process. We say this knowing that real estate investors are out all day at projects or scoping out new acquisitions — not in front of a computer like mortgage brokers, private lenders, and title and escrow officers.

But if you can get your documents in order, and have them at your fingerprints on your computer or phone, you've done yourself a huge favor by smoothing the path to approval.

A little preparation upfront will pay off in the end.

Real estate investors have their choice of several private money lenders to help them acquire and renovate their next fix and flip project. However,...

If you’re cash strapped and in escrow to purchase your next fixer-upper, you might be searching online for a hard money lender to give you the...

If you've always wanted to flip houses and just found a great deal on a fixer-upper that would make a perfect flip, your next step is to find the...