Ted Spradlin

Ted Spradlin

Loan Scenario – 85/15 Seller Financing Plus Hard Money Second Mortgage

A homebuyer secured a seller-financed first mortgage at 85% Loan-To-Value (LTV) and asked if FCTD could provide a hard money second mortgage for the...

During the second half of 2023, a number of commercial real estate investors have inquired with FCTD about getting hard money second mortgages, to be used in the same manner as a preferred equity investment. They planned to use the additional liquidity to secure the senior debt position on their property — whether a 5-year mortgage about to reach maturity, or a construction loan on a newly built apartment building. Each situation required an injection of capital, to complete the “cash-in refinance” on the new first mortgage.

And for reasons I'll discuss, preferred equity investments — a solution typically used for these situations — have become difficult to come by, causing these investors to explore hard money second mortgages as an alternative.

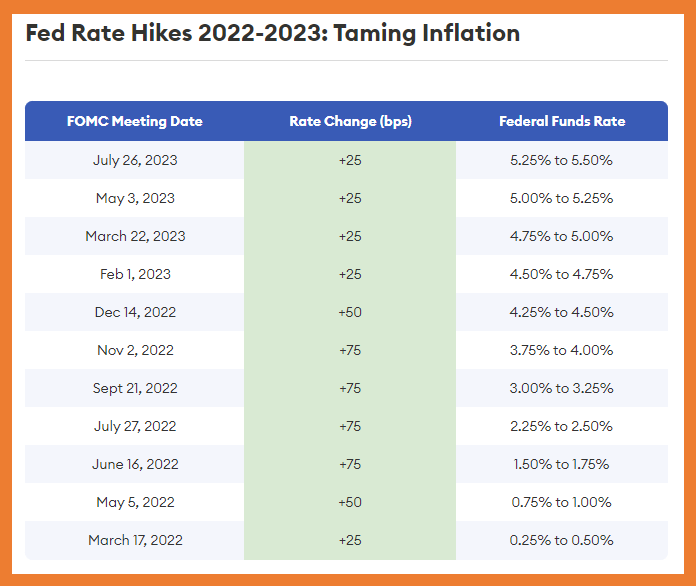

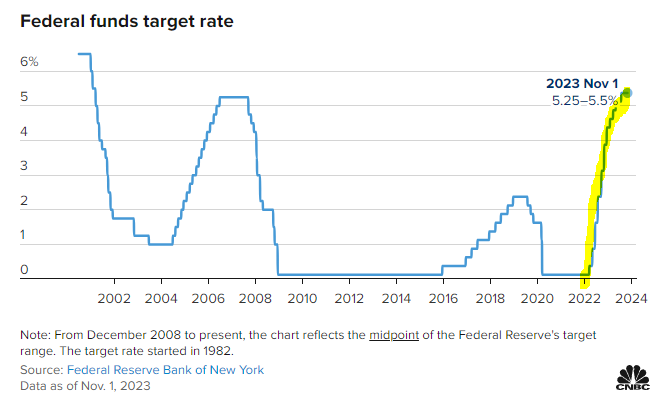

The uptick is directly tied to the rapid rise in the Federal Funds Rate, which has gone from 0.25% in March 2022 to 5.50% in July 2023.

Chart: Federal Funds Target Rate (CNBC)

During the past 18 months, debt has become much more expensive, while the amount that real estate investors can borrow has significantly decreased.

It’s common in today’s market for an apartment developer with a maturing $10 million construction loan to provide $1 million “cash-in” to refinance into a long-term mortgage for $9 million at 7.50%. Many developers don't have $1 million available. They usually have multiple projects at different points of development, with available cash on hand designated for those projects.

This liquidity gridlock playing out in the commercial real estate market is causing the uptick in requests for preferred equity investments and hard money second mortgages.

Chances are, if you’re a real estate investor reaching out to hard money second mortgage lenders, you've already checked with potential preferred equity investors in your network, many of whom are taking a wait-and-see approach to the real estate market. They’re noticing the headlines or have had firsthand experience with their own real estate investments — and are proceeding with caution or waiting on the sidelines.

There are many informed opinions on where we are in the real estate cycle, so it’s hard to tell where any one investor stands.

To bring clarity to this moment in time, I'll go into the details of both hard money second mortgages and preferred equity investments, covering the following topics:

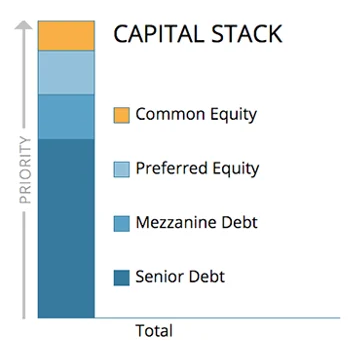

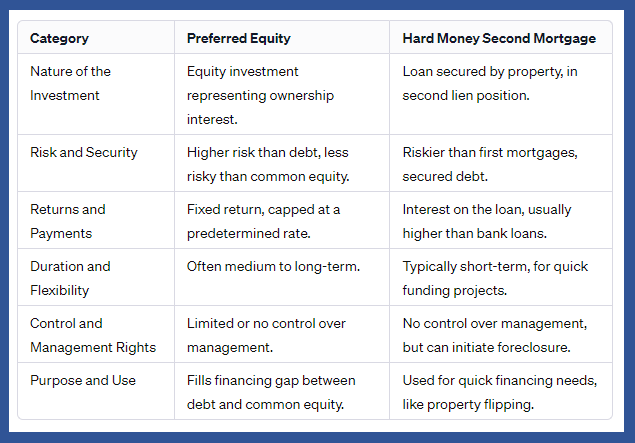

Preferred equity is a financial instrument in real estate investing used to bridge financing gaps for the borrower, while providing an investment for the lender that balances risk with reward.

You can see from the capital stack chart above, preferred equity lies between common equity and debt. This means that when a property is sold or refinanced, preferred equity holders are paid after debt holders but before common equity investors.

Investors in preferred equity typically receive fixed returns, which are higher than those offered to debt investors but lower than the potential returns on common equity. They also generally have priority in cash flow distributions over common equity investors. However, that return is capped unlike with common equity.

Preferred equity investors usually have limited to no management rights in the property. Overall, it's a hands-off position, with some elevated risk — but if all goes well, it can generate higher returns.

Hard money second mortgages are junior liens secured by real estate and usually issued by a private lender rather than a bank or conventional lender. The “second” means that the mortgage is subordinate to the senior lien encumbering the property, also called the “first” mortgage. If the borrower defaults on the first or second mortgage and the property is sold through foreclosure auction, the first mortgage is repaid before the second.

Also known as private money loans, hard money second mortgages are debt. The lenders don't have any interest in the gain or decline in value. The loan is simply debt that will need to be repaid on or before a specific date, known as the balloon payment.

Hard money loans are made by individual trust deed investors, family offices, real estate investment firms, mortgage funds, and conduit lenders. These lenders will usually limit the Combined Loan-To-Value (CLTV) on hard money second mortgages to 65% CLTV, give or take —depending on property type, location, and borrower strength and experience.

However, in California, where FCTD and most of our borrowers and lenders are based, we'll consider a second trust deed at 70% CLTV if the scenario makes sense. In contrast, in Q4 2023, many hard money lenders are pulling back on second mortgages in Florida, due to the overheated market and concerns about rising insurance costs.

FCTD’s primary focus as a mortgage broker is originating debt rather than placing equity investments.

Our trust deed investors work with us to provide them with a steady flow of private mortgage financing options, where they can earn a desired yield while having a layer of protective equity between their lien and the market value of the property.

Most of the private lenders FCTD works with have extensive background in real estate and finance. Some have invested as limited partners (LPs) in real estate syndications while others have been the general partner (GP) in one or more syndications. They work with us because they want a portion of their investment funds in private money loans to complement their real estate investments.

That being said, if you have a preferred equity investment proposal, it doesn't hurt to run it by us. You, as a sponsor, and your investment opportunity may be a good fit with one of our long-time trust deed investors.

We’ve also referred several real estate investors to other mortgage professionals in our network, whose focus is commercial institutional lending with banks, credit unions, CMBS, and life company financing.

Working Together on Debt Placement and Private Money Loans

The unique challenges of the current moment may make it more difficult to get the preferred equity investment or hard money second mortgage you're after for your commercial real estate project. At FCTD, we have our finger on the pulse of the industry and understand the challenges investors like you experience during cycles of change and adjustment. Even if there isn't a current fit for a hard money second mortgage or preferred equity investment, reaching out to FCTD now is a good way to make a connection with a well-resourced mortgage brokerage that may be able to help serve your future needs.

A homebuyer secured a seller-financed first mortgage at 85% Loan-To-Value (LTV) and asked if FCTD could provide a hard money second mortgage for the...

I had a loan scenario come in through the website in 2022 where a non-military veteran was assuming a Veterans Administration (VA) loan, and needed a...

If you’re trying to estimate the costs for a hard money second mortgage, we've got you covered with this blog post on pricing, closing costs, terms...